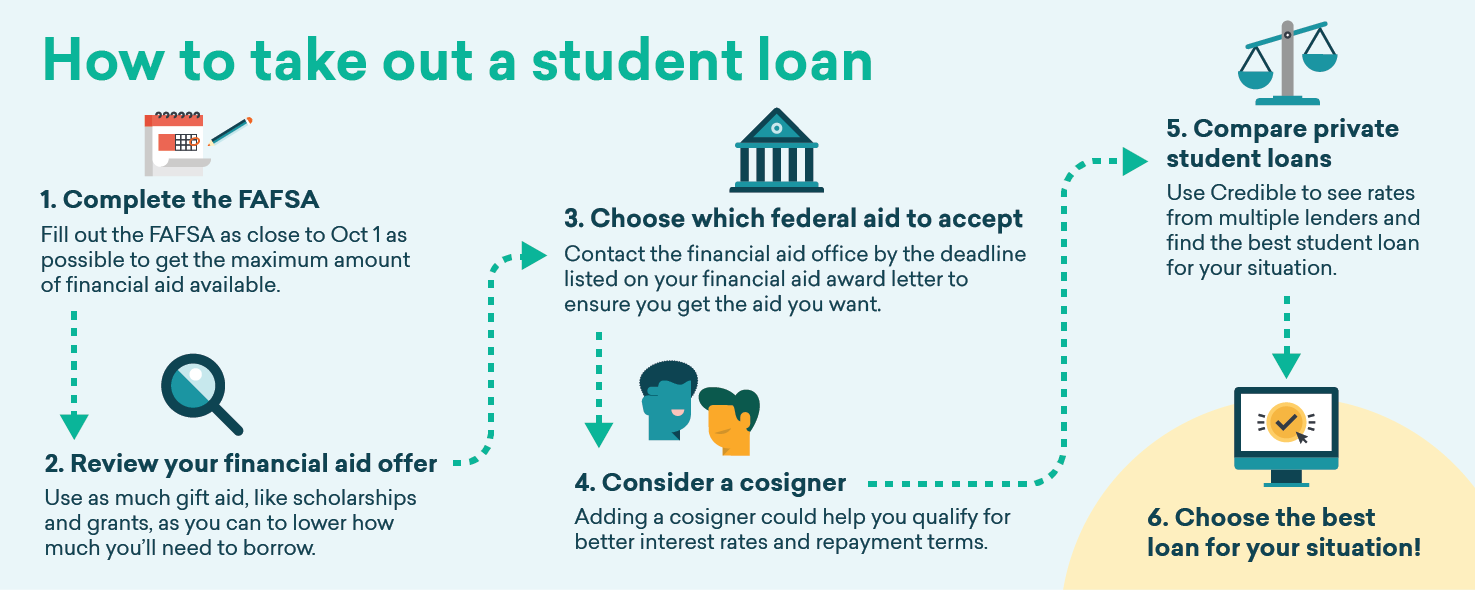

When students pursue higher education, the financial burden can often feel overwhelming. Many opt for student loans to cover tuition and living expenses, but what happens once those loans are approved? The process involves signing a formal agreement that lays out the terms and conditions of repayment. This document is crucial for understanding the responsibilities that come with borrowing money for education. In this article, we will delve into what this signed agreement is called, its significance, and the implications it has for students.

As you navigate through the complexities of student loans, it is essential to grasp the terminology and processes involved. Knowing what to expect and understanding the nuances of the signed agreement can empower you to manage your finances more effectively. Whether you are a first-time borrower or considering additional loans, having clarity on these matters is vital for your financial health and future.

In addition to the specifics of the agreement, we will explore common questions and concerns that arise when taking out student loans. From understanding interest rates to repayment options, this comprehensive guide aims to equip you with the necessary knowledge to make informed financial decisions as you embark on your educational journey.

What Is the Signed Agreement Called When Taking Out Student Loans?

The signed agreement that borrowers enter into when taking out student loans is commonly referred to as a "promissory note." This legal document serves as a binding contract between the borrower and the lender, outlining the terms of the loan, including the amount borrowed, interest rates, repayment schedule, and any penalties for failure to adhere to these terms.

What Are the Key Components of a Promissory Note?

A promissory note contains several critical components that borrowers should understand:

- Loan Amount: The total amount of money being borrowed.

- Interest Rate: The percentage of the loan that will be charged as interest.

- Repayment Terms: The timeline for when repayments are due and the length of time for repayment.

- Loan Servicing Information: Details about who will manage the loan and receive payments.

- Default Consequences: The penalties for failing to repay the loan on time.

How Is the Promissory Note Different from Other Loan Agreements?

While a promissory note is a type of loan agreement, it is specifically tailored for educational loans. Unlike other loan agreements, it often includes provisions for deferment or forbearance, allowing borrowers to temporarily pause their payments under certain circumstances, such as returning to school or facing financial hardship.

Why Is Understanding the Promissory Note Important?

Understanding the promissory note is crucial for several reasons:

- Financial Responsibility: Knowing what you are agreeing to helps you manage your finances responsibly.

- Avoiding Surprises: Being aware of the terms can prevent unexpected charges or penalties.

- Informed Decisions: Understanding the implications of the agreement allows you to make informed decisions about your education and finances.

What Should You Do Before Signing a Promissory Note?

Before signing a promissory note, consider the following steps:

- Read the Document Thoroughly: Ensure you understand all terms and conditions.

- Ask Questions: If anything is unclear, do not hesitate to ask the lender for clarification.

- Compare Options: Explore different loan options to find the best terms for your situation.

What Happens After You Sign the Promissory Note?

Once you sign the promissory note, the lender will disburse the loan funds, often directly to your educational institution. It is essential to keep a copy of the signed note for your records, as it will be a vital document throughout your repayment journey.

What Are the Consequences of Defaulting on a Student Loan?

Defaulting on a student loan can have serious implications, including:

- Damage to Credit Score: Defaulting can significantly lower your credit score, affecting your ability to borrow in the future.

- Collection Actions: Lenders may take legal action to recover the funds, which could lead to wage garnishment or tax refund interception.

- Loss of Financial Aid: Defaulting may make you ineligible for further federal student aid.

How Can You Avoid Defaulting on Your Student Loans?

To prevent default, consider the following strategies:

- Stay Informed: Keep track of your loan balance and repayment schedule.

- Communicate with Your Lender: If you’re struggling, reach out to discuss your options.

- Explore Repayment Plans: Look into income-driven repayment plans that can make payments more manageable.

What Resources Are Available for Student Loan Borrowers?

Several resources can assist borrowers in managing their student loans:

- Federal Student Aid: Offers information on repayment options and loan forgiveness programs.

- Financial Aid Office: Your school’s financial aid office can provide guidance and support.

- Credit Counseling Services: Non-profit organizations can help you understand your loans and create a repayment strategy.

Conclusion: Navigating the Student Loan Agreement Process

Understanding what happens when taking out student loans, specifically the signed agreement known as the promissory note, is crucial for any borrower. This document outlines your responsibilities and the terms of your loan, serving as a roadmap for repayment. By familiarizing yourself with the components of the promissory note and the implications of your agreement, you can make informed decisions that will positively impact your financial future. Remember, staying proactive and informed is key to successfully managing your student loans and avoiding potential pitfalls.